Julian Robertson, 90, Dies; Brought Hedge Funds Into the Mainstream

Julian Robertson, a Wall Street investor who with a handful of others pushed short-selling into the mainstream, helping to create the modern hedge fund industry, died on Tuesday at his home in Manhattan. He was 90.

His son Alex said the cause was cardiac complications.

Two years before abruptly closing down his pre-eminent Tiger Management Corporation investment stable in 2000, Mr. Robertson was overseeing some $22 billion in a half-dozen funds containing a wide assortment of long and short positions in stocks, bonds, commodities and currencies from around the globe.

He continued to manage his own multibillion-dollar fortune well into his 80s.

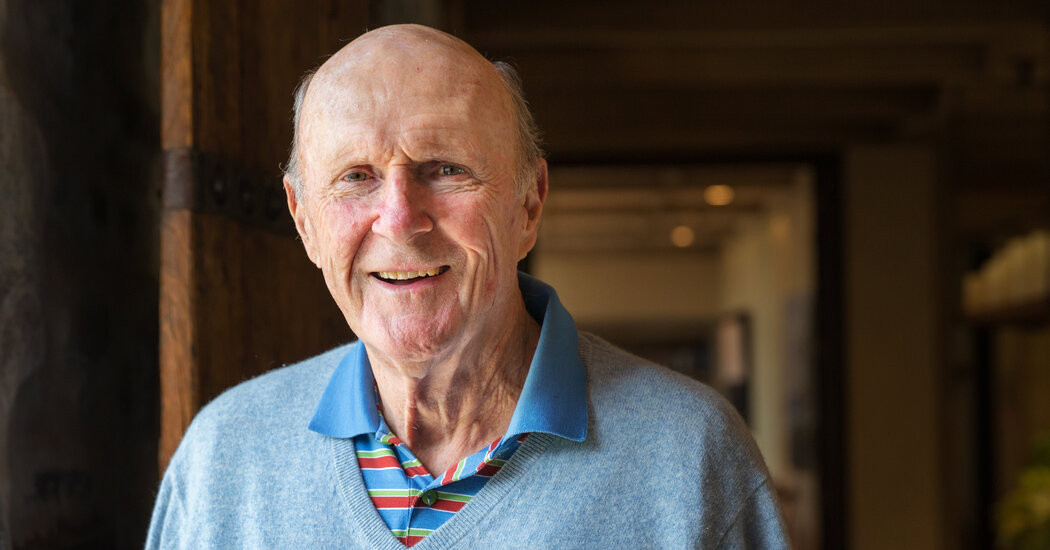

A courtly and smartly tailored North Carolinian, Mr. Robertson was not only a champion investor — a Business Week cover once hailed him as “the best stock picker on the Street” — but also a mentor to several dozen hedge fund progeny. His legacy included traders known as Tiger “cubs,” who started in his employ and then went out on their own, and Tiger “seeds,” whose budding funds he supported with investment.

“Julian Robertson is one of the few hedge fund managers I admire as much for the way he’s used his money as for the way he made it,” George Soros, the most prominent of the hedge fund pioneers, said in 2016, referring to his philanthropy as well as his investment culture.

James S. Chanos, a renowned short-seller who managed money for the three 1980s hedge fund titans — Mr. Robertson, Mr. Soros and Michael H. Steinhardt — was quoted in Sebastian Mallaby’s industry history “More Money Than God: Hedge Funds and the Making of a New Elite” (2010) as saying that if he were to “give my own money to any of them, I would have given it to Robertson.”

The heart of Mr. Robertson’s investment strategy was to try to eliminate the risk of general market swings by shorting stocks — making investments premised on the bet that a company’s stock will fall. Though the practice had been employed for centuries, Mr. Robertson made it a central element of his trading.

“Our mandate is to find the 200 best companies in the world and invest in them and find the 200 worst companies in the world and go short on them,” he would explain. “If the 200 best don’t do better than the 200 worst, you should probably be in another business.”

Finding undervalued or overvalued companies was crucial, but as Tiger’s outstanding results swelled its assets, he began to trade more frequently. He eventually took account of broad economic and political developments as well. He diversified into commodities, and at one point he was reputed to control nearly a year’s output of the world’s supply of palladium, a metal used in automotive catalytic converters.

From Tiger’s inception in 1980 to its 1998 asset peak, Mr. Robertson produced annual returns averaging 31.7 percent after fees, dwarfing the 12.7 percent rise in the Standard & Poor’s 500 stock index over the same period. Tiger showed losses in only four of its 21 years.

These returns poked holes in the so-called efficient market theory, which holds that market prices immediately reflect all known information, making it impossible to outperform the market consistently.

Julian Hart Robertson Jr. was born on June 25, 1932, in Salisbury, N. C., the son of a textile executive he said was descended from Pocahontas. His mother, Blanche, was a local activist whom the mayor called the city’s “biggest cheerleader.”

A mediocre student but a self-described “geography nut,” he graduated from the University of North Carolina at Chapel Hill, where he was in the Reserve Officers Training Corps, and then served two years in the Navy traveling the world aboard a munitions ship.

It was there, he said, that he developed leadership skills when, as a lieutenant junior grade, he was often put in charge of the ship on weekends.

After the Navy, “I was pretty happy to stay in North Carolina,” Mr. Robertson recounted in a 2016 interview for this obituary.

If he stayed, however, he probably would have managed textile mills. If he wanted to make money, he said, “My father felt strongly that I should go to New York.”

He started as a sales trainee at Kidder, Peabody & Company and worked his way up through the brokerage ranks while building a reputation for finding bargain stocks. But in 1978, tired of the related marketing chores, Mr. Robertson decided to take a sabbatical of sorts.

He took his wife and their two young sons to New Zealand. “I thought I could write the great American novel,” he said in 2016.

The writing project, which he came to call “narcissistic,” foundered, and his sister Wyndham Robertson, a journalist at Fortune magazine, persuaded him to abandon it.

But he had fallen in love with New Zealand — he said it had the greatest geography for its size in the English-speaking world — and that attachment led him, years later, to create three major resorts there, spurring the country’s tourist industry.

His purchase of one site, the 4,800-acre Lodge and Golf Course at Kauri Cliffs, was, he said, the equivalent of buying California’s Pebble Beach golf course for the price of a modest apartment in New York. After its opening in 2000, it was named one of the five best courses in the world by Golfweek magazine.

Returning to New York, Mr. Robertson decided to leave his 22-year Kidder, Peabody career behind and make his own mark on Wall Street by creating Tiger Management with an $8 million stake of his own money and friends’.

“I had become convinced that the hedge fund was the way to invest,” he recalled, and that short-selling was “a license to steal.”

Mr. Robertson prospered, but in the mid-1990s his performance grew ragged amid the mania for untested dot-com stocks. Investors withdrew, and in 2000 a baffled Mr. Robertson, his strategy no longer working, closed shop.

“There is no point in subjecting our investors to risk in a market which I frankly do not understand,” he told investors.

In a 2004 biography, “Julian Robertson: A Tiger in the Land of Bulls and Bears,” Daniel A. Strachman quoted Mr. Robertson as saying, “The mistake that we made was that we got too big.” This meant, he added, that “to make it meaningful we had to buy a huge amount of a company’s stock, and there were only a few companies” where that was an option.

Others said that Mr. Robertson’s autocratic style, increased competition and heavy speculative losses in shares of US Airways and in the Japanese yen contributed to the company’s demise.

In addition to his son Alex and his sister Wyndham, Mr. Robertson is survived by two other sons, Spencer and Julian III, and nine grandchildren. Another sister, Blanche Robertson Bacon, died in 2021.

Among Mr. Robertson’s numerous philanthropies are 36 full scholarships shared each year since 2000 by students at the University of North Carolina and Duke University. Memorial Sloan Kettering’s Josie Robertson Surgery Center and Lincoln Center’s fountain plaza both honor his wife, Josephine (Tucker) Robertson, whom he married in 1972 and who died in 2010.

Although underlings sometimes found Mr. Robertson single-minded and hypercompetitive, he said it would “thrill” him to be remembered for giving his money away. A statement by his publicist said that over his lifetime he contributed more than $2 billion to charity.

Most certainly, he insisted, “I didn’t want my obituary to read, ‘He died getting a quote on the yen at 2 a.m.’”