How Long Does It Take to Save Up for a Down Payment?

The biggest barrier to homeownership for many prospective buyers isn’t the monthly mortgage bill, but the steep down payment. The 20 percent required to qualify for a typical mortgage for a median-price home in the United States (roughly $455,000) comes to about $91,000 — a formidable stack of cash.

Saving that much would take years for most households, but a recent study by RealtyHop dug deeper, comparing local median home prices and incomes to locate where a down payment could be compiled quickest. Some 1.8 million RealtyHop listings were examined in the 150 largest U.S. metro areas, and a saving rate of 20 percent of gross income per year was applied to the formula. Single-family homes, townhouses, condos and co-ops were included.

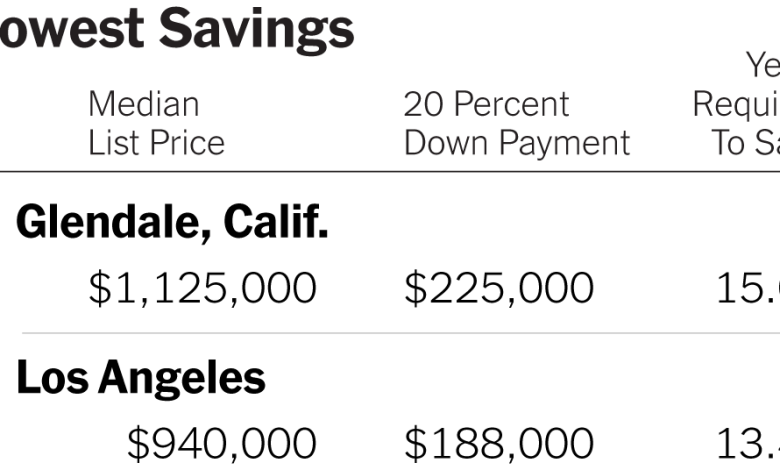

It’s not as simple as earning more, because the places where households earn the most also tend to have the highest home prices. Consider San Francisco, where the median household earning $126,187 a year would need 10.5 years to save the required $265,000 down payment for a median-price home costing $1.325 million. Three other California metros — Long Beach, Los Angeles and Glendale — require even more time to save.

But it doesn’t take a decade everywhere. In one third of the 150 metros, saving up for a down payment would take less than five years. If you’re in a hurry, consider Detroit, the metro where savings were found to build quickest. There, the median household earning $34,762 would need just two and a half years to save up a $17,780 down payment for the median-price home costing $88,900.

This week’s chart, based on RealtyHop’s data, shows the 10 metros where saving up would be fastest and the 10 where it would be slowest.

For weekly email updates on residential real estate news, sign up here.